This article was first published on LinkedIn on March 21, 2025. Link to original article.

Small Rockets - a Brave Investment!

Back in 2021, I wrote a LinkedIn article titled The Rocket Bubble about the companies developing small launch vehicles. There were 126 of them at the time. I came to 4 conclusions:

- Fewer than 20 had any realistic chance of reaching orbit.

- Launch costs had fallen dramatically, undermining the business cases for many small launch vehicles.

- The market for small rockets was much smaller than claimed.

- I advised investors to focus on companies using satellites to deliver valuable services, driving launch demand, rather than capital-intensive launch providers with limited return potential.

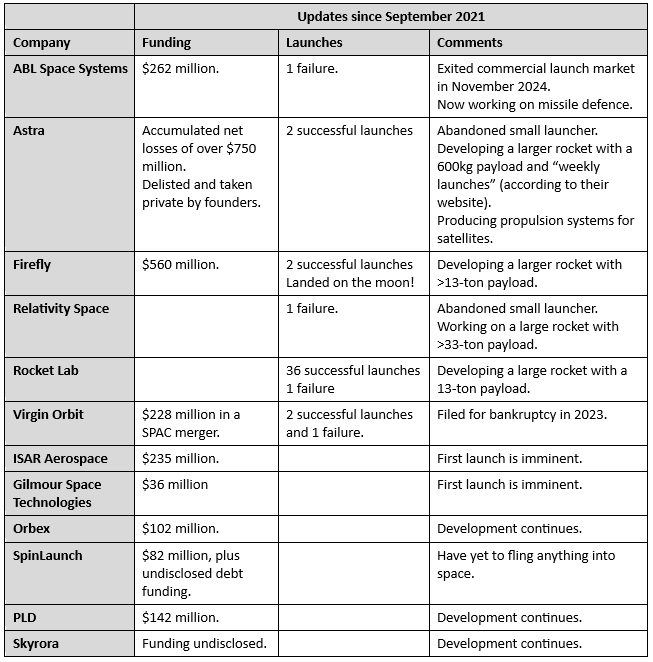

I identified 20 active companies (plus one that had already failed) that had raised at least $20 million by September 2021:

Three Years Later: Reality Check

Three years on, how are those companies doing? Are they all launching satellites, as most had promised they would by now?

Spoiler alert: they are not!

Let's look first at the 12 non-Chinese companies:

- An additional $1.6 billion has been invested since September 2021.

- 6 of the 12 are still in the development phase.

- 4 have completely abandoned small launch vehicles, or declared bankruptcy.

- Only Rocket Lab delivers regular launches, yet even they are pivoting toward larger rockets to improve returns.

- Firefly has launched successfully twice and plans to continue, but it too is now developing a larger rocket to generate better returns.

Here's the detailed update:

The four companies that abandoned small rocket development have been replaced by several more that have raised substantial funding since my 2021 article, including Rocket Factory Augsburg (Germany), HyImpulse (Germany), Latitude (France), MaiaSpace (France - subsidiary of Ariane Groupe) and Skyroot (India) - all of which are making rapid technical progress. Sadly, they will not all succeed.

Despite the billions invested, only Rocket Lab provides a reliable launch service, and even it struggles to generate significant profits from launch services. Meanwhile, the other companies are grappling with intensifying competition as launch costs for larger rockets fall still further, and commercial demand for relatively expensive small rockets remains low.

As global politics grow increasingly volatile, many national governments urgently seek dependable launch capabilities free from political risks. But while governments may back rocket developers, they won't buy enough launches to guarantee commercial success. Investors should be very cautious about following the lead of governments.

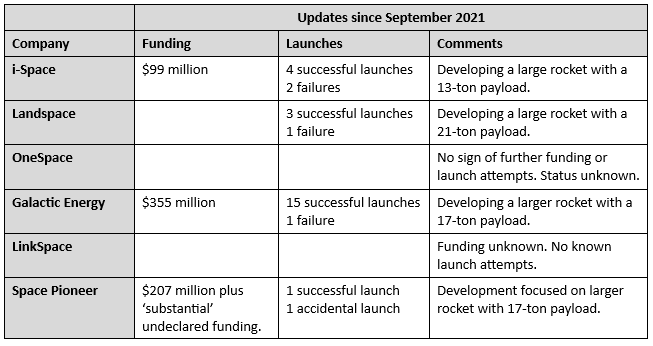

How about the Chinese rockets?

ExPace is 100% state owned so probably shouldn't have made the original list, and Space Transportation is fully focused on developing a space plane (good luck with that...), so doesn't compete in the same market. Among the remaining Chinese companies:

- A further $660 million has been invested since September 2021.

- Collectively, 4 companies have completed 23 successful launches, 4 failed launches, and the world's first accidental launch. (A note to rocket owners: check the retaining bolts before testing your rocket's engines on the pad!).

- All active companies are shifting their focus toward larger rockets.

- The status of two companies remains unclear.

Here's how they stand now:

The situation for Chinese companies mirrors that of their global counterparts. Significant funds have been invested with uncertain returns, and even more investment is required. All companies are rapidly shifting their focus to larger rockets, where they anticipate better financial returns.

Conclusion: Persistent challenges, limited returns

Three years on from my previous article, despite an additional ~$3 billion invested in small rocket development, not a lot has changed.

Some high-profile companies have failed, or moved on to new projects. Some enthusiastic newcomers have replaced them, confident that they will do better. Meanwhile, commercial launch costs have continued to fall, and profitable small satellite operators, who might drive demand, remain scarce.

The need for countries to secure reliable access to space in an uncertain world is greater than ever, which will surely benefit some of the new launch companies. But the limited demand for relatively expensive launches of small satellites will not be sufficient for them to operate profitably and recoup their development costs. Investors who were betting on substantial equity returns will lose their bets.

About the Author: Adrian Norris

Adrian Norris is an aerospace advisor with over 30 years of international experience spanning strategic consulting, aviation and space startups, aircraft development and certification, and corporate leadership. He works with investors, founders, and executives to shape strategy, assess feasibility and risk, and distinguish real opportunities from industry hype. He was the co-founder of a satellite imaging company. Based in France and the UK, he holds a Master's degree in Leadership & Strategy and brings a unique blend of technical and commercial insight to the aerospace industry.