This article was first published on LinkedIn on October 13, 2025. Link to original article .

BETA Technologies' IPO

BETA Technologies has filed for an IPO. The share price and number of shares offered have not yet been disclosed, but a preliminary prospectus filed with the SEC gives interesting information about the company.

Should you invest? Let's look at the arguments for and against.

Why people may want to invest

There are some good reasons why people may want to participate in BETA's IPO:

- BETA made a sensible pivot, focusing on an eCTOL aircraft (Conventional Take-off & Landing) before the eVTOL they originally planned. The CTOL aircraft will be far easier to certify while retaining significant commonality with the future VTOL variant.

- The CTOL aircraft has enough payload and range for some commercial missions. I saw it fly at the Paris Airshow, and have spoken to people who've flown it. It appears to offer a credible basis for certification.

- GE Aerospace is investing $300 million in BETA. They probably did thorough due diligence.

- UPS, Air New Zealand and Bristow have all placed orders. They probably did their due diligence too.

- BETA has raised significant funding. The total is not disclosed, but it is reported to be around $1.7 billion in equity, debt and grants.

- Kyle Clark, BETA's founder and CEO, appears to be an impressive leader. He has grown his company rapidly, and people at BETA speak highly of him.

- BETA has an aviation culture. Kyle Clark is a pilot, and every employee has access to the company flight school. I think that's a good thing in an aircraft company.

Why rational investors should be very wary

The positive points may attract people, but I believe they are outweighed by some serious concerns, which I have grouped into 4 categories:

1. The Aircraft

- Performance is marginal: 1,240 lb payload, 215 mile range, 1 hour battery recharge time between flights, unable to operate in icing conditions. This compares unfavourably with much cheaper conventional aircraft. It will be extremely hard for operators to make money with BETA's aircraft.

- While BETA has agreed the Certification Basis for their aircraft (FAA 'G-1' Issue Paper), they have not yet announced agreement of the Means of Compliance (FAA 'G-2' Issue Paper). BETA expects to receive a Type Certificate in late 2026 / early 2027, but this is an optimistic target. Investors should anticipate a delay.

- BETA expects to receive a Type Certificate for the VTOL variant in late 2027 / early 2028. I think this is very optimistic.

- Pricing has not been announced, but data in the prospectus suggests a unit price above $3 million, and perhaps above $4 million. That is comparable to a turboprop Cessna Caravan, which is a far more capable aircraft.

- Aircraft batteries will need replacement every 12-24 months.

- BETA explicitly sees the battery as a way to make money, with high margins. Here are some quotes from the prospectus:

if operated for 20 years, we estimate a typical electric aircraft will require 18 to 20 sets of replacement batteries, generating approximately $13 million in revenue

Battery replacements alone are expected to exceed the initial revenue from selling individual aircraft and provide higher margins

Our business strategy centers around leveraging aircraft sales to generate extensive recurring revenue at attractive margins over the lifetime of each aircraft

- Customers will not buy an expensive aircraft with limited capability, which requires them to spend roughly three times the purchase price on new batteries over 20 years.

2. The Market

BETA initially planned to serve the market for urgent medical logistics market with its eVTOL aircraft. This is an extremely small market today, but an early investor and launch customer, United Therapeutics, anticipates rapid growth in demand linked to its organ transplant activities.

The company now plans to prioritise cargo and logistics, along with defence (the prospectus describes a future military eVTOL variant) and passenger transport.

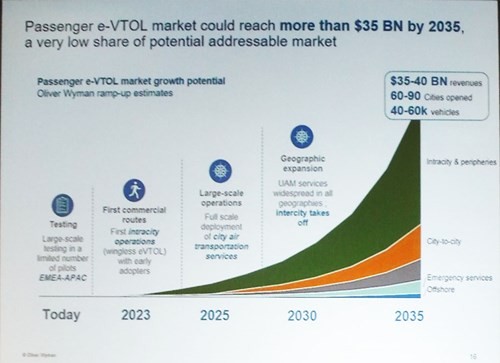

- BETA estimates a Total Addressable Market of 60,000 electric / hybrid aircraft by 2035. They cite "analysis conducted by a global third-party consulting firm”. I have looked hard for this, and the only matching figures I have found are from an Oliver Wyman study in 2019 - which has since proven to be wildly optimistic:

- BETA also claims that its aircraft is “well suited for emerging necessities of modern warfare” and that helicopters “are poorly suited for imminent threats”. It is not plausible that military operators will replace helicopters with electric aircraft that carry less payload, have shorter range, and require a high-voltage charging infrastructure.

BETA's market size assumptions appear exaggerated, and its expectations for market penetration are unrealistically high.

3. Governance and control.

Perhaps the most concerning issues relate to BETA's corporate governance, and the absolute control by Kyle Clark. He may be a splendid person, and I fully understand why he would want to keep full control of his company at this stage. But...

- Kyle Clark’s Class B ‘super-voting’ shares carry 40 votes each.

- Class A shares (sold to the public) carry 1 vote each.

- Kyle Clark’s 1.33 million shares (~53 million votes) outvote all other shareholders combined.

- Forty votes per share is unprecedented. Google and Meta founders have 10. WeWork’s CEO initially gave himself 20 (not a great reference). BETA has 40, with no sunset mechanism.

- Kyle Clark has the right to designate a majority of the board, and to veto changes to the board size.

- BETA qualifies as a “Controlled Company” and openly declines to meet NYSE governance standards.

- IPO investors will have no power to influence the company.

4. Use of funds and executive spending

BETA Technologies is a high-risk, pre-revenue company with over 800 employees, high cash burn, and uncertain future revenue size and timing. It has an aircraft certification project underway which will be hugely expensive. So investors have the right to expect extremely cautious use of their IPO funds. But...

- Executive pay will surge at IPO. Kyle Clark’s compensation will increase from $530k to $815k per year, and his bonus will increase from 100% (fully earned in 2024) to 200% of base salary.

- $10 million of IPO proceeds will be used to pay cash bonuses to Kyle Clark and "certain employees".

- BETA purchased a business jet from one of its Directors for $7.25 million. (Kyle Clark now has a type rating to fly the jet.)

- BETA leases a house owned by Kyle Clark for use "as temporary housing to certain of our employees". The lease payment was $133k in 2024.

If BETA starts making money, substantial rewards for executives will be fully justified - in addition to their significant share ownership. Until then, they should be fairly paid but every spare dollar should be directed to engineering and certification. But that is not how BETA is run.

Conclusion

I'd always rather liked BETA Technologies. While some eVTOL companies made exaggerated claims, BETA quietly got on with building a usable electric aircraft. I'd like them to succeed, but it's impossible to recommend investing in this IPO.

The aircraft has marginal capability, high cost, and prohibitively expensive battery replacements. The founder will retain absolute and unquestionable control of the company, for as long as he chooses. And too much money is being spent on the wrong things, even if the amounts are small compared to BETA's total funding.

Perhaps there will be a revised prospectus that is more attractive. Until then, steer clear.

Update: February 12th 2026

- The prospectus was not substantially modified before the IPO on November 4th 2025.

- The IPO raised over $1 billion, providing substantial liquidity to BETA.

- In the 100 days after the IPO, the share price fell by over 50%.

About the Author: Adrian Norris

Adrian Norris is an aerospace advisor with over 30 years of international experience spanning strategic consulting, aviation and space startups, aircraft development and certification, and corporate leadership. He works with investors, founders, and executives to shape strategy, assess feasibility and risk, and distinguish real opportunities from industry hype. He was the co-founder of an aircraft development company in the US and is a licensed commercial pilot. Based in France and the UK, he holds a Master's degree in Leadership & Strategy and brings a unique blend of technical and commercial insight to the aerospace industry.

Contact

Get in touch to discuss a current project or investment.

We provide independent, evidence-based analysis to support investment and strategic decisions.