This article was first published on LinkedIn on July 25, 2025. Link to original article .

What's going on with eVTOLs?

Three leading eVTOL companies announced successful demonstration flights this month.

Joby has been flying in Dubai (sending its share price rocketing), Archer have flown their aircraft in nearby Abu Dhabi, while in the UK Vertical Aerospace claim to have achieved the world’s first “public airport-to-airport flight” by an eVTOL.

News of Archer’s demonstration flights couldn't prevent a judge from allowing a lawsuit by disgruntled shareholders to proceed. They believe the company’s progress was exaggerated prior to its SPAC merger in 2021.

The trial will determine whether Archer did exaggerate. But murmurings of discontent about the slow progress of all three companies are becoming louder. Why are they taking so long to bring their aircraft to market? And a follow-on question: is the market really as big as they say?

Let’s look into it!

Certification, Certification, Certification!

Before looking at each company’s progress, it’s important to understand the process by which aircraft are certified. For investors interested in aviation projects, nothing is more important than aircraft certification. It is the rock on which many unrealistic projects founder.

I’ll outline the FAA process followed in the US by Archer and Joby. Vertical Aerospace has to follow essentially the same rules in the UK, but the process is slightly different.

The process can be broken into five phases, with defined milestones that need to be approved before moving to the next phase.

- Conceptual design of the aircraft, initial engagement with the FAA, resulting in an application for a Type Certificate.

- Establish the Certification Basis for the aircraft. This defines the certification rules and ‘Special Conditions’ that need to be followed. Special Conditons are additional rules added when existing regulations don’t fully cover a new or unique design feature.

- Agree the Project Specific Certification Plan (PSCP). This defines how the Certification Basis will be met, referred to as the 'means of compliance'. It defines the required tests, which decisions the FAA will make, what can be delegated to FAA-approved company engineers, necessary inspections, and much more.

- Implement the PSCP. This involves ground and flight testing, submitting test plans and test results to the FAA, and resolving all the issues that arise. Or, in other words, demonstrating compliance with the Certification Basis.

- The final phase involves FAA test pilots flying aircraft that are identical to production aircraft, known as 'conforming prototypes'. When this is completed successfully, the FAA issues a Type Certificate.

These phases can overlap. For example, testing (phase 4) can take place before the PSCP is agreed (phase 3), but the FAA will not formally approve test results, so there is a risk of wasted effort. Companies can make a lot of progress on the 'easy' parts of certification before agreeing the PSCP, but agreeing the whole plan can be very difficult for a novel aircraft design.

So, how are the eVTOL companies’ certification projects progressing?

Archer

In 2021, Archer announced: “we have agreed with the FAA on the certification basis for our eVTOL aircraft. We continue to work with the FAA on the means of compliance for that certification basis”. (See page 48 of link.)

So far, so good.

Then, in the 2024 annual report, they announced: “in June 2024, we then finalized our certification basis with the FAA. We are continuing to work with the FAA to agree on the Means of Compliance”. (See page 4 of link).

Deciphering that, they hadn’t agreed the PSCP by the end of 2024. No subsequent announcements suggest that they have, so they certainly still have a long way to go.

Joby

In 2021, Joby announced: “While we have agreed with the FAA on the basis for our type certification (…), we still are in the process of testing and refining our designs (…). This process is expected to continue through at least 2023.” (See page 44.)

In the same SEC filing, they announced: “we are well on our way towards certification and engage with the FAA on a daily basis to perform the hard work and testing required to earn FAA type certification prior to our 2024 commercial launch goal.” (See page 50.)

One might reasonably conclude that the Certification Basis had been agreed, with certification expected in 2023 and commercial launch in 2024.

In February 2024, when we were expecting that “commercial launch”, a Joby press release announced that "Joby has now completed three of five stages of type certification process; First eVTOL company to reach this milestone towards commercialization".

Joby’s ‘five stages’ are an internal definition. But they are defined in their SEC filings (see page 8) as follows:

- Define the Certification Basis

- Identify the Means of Compliance

- Develop detailed certification plans to satisfy the means of compliance. (Note: this implies agreement of the PSCP.)

- Testing and Analysis. (i.e. implementation of the PSCP)

- FAA verification of results from Stage 4, leading to issue of a Type Certificate

So, as that February 2024 press release said that three stages had been "completed", one might assume that the PSCP had been agreed.

However, in an SEC filing in October 2024, Joby said: “We think of the FAA type certification process in five stages and have made significant progress towards certification. We have completed or substantially completed three of these five stages.” (See page S-1.)

“Substantially completing” something by October 2024 is not quite the same as actually completing it by February 2024. As the company is not being entirely transparent, some speculation is in order. I speculate that they haven’t agreed their PSCP, and that they have a long way to go!

Nevertheless, a press release following the demonstration flights in Dubai in June said: “these efforts will further develop Joby’s readiness in anticipation of carrying its first passengers in 2026”, so they must be optimistic that they will soon agree the PSCP and then finish the implementation phase very quickly. I don’t have any inside information, so they could be right – but it would be very unusual for such a complex certification project to progress that quickly after spending so many years working towards the PSCP.

Vertical Aerospace

- In 2021, they promised certification, full production, and "significant revenue generation" by 2024.

- In 2021, in SEC filings at the time of their SPAC merger, they expected certification by 2024.

- In 2022, they announced that they expected certification in 2025. (See page 10.)

- In 2023, they expected certification in 2026.

- In 2024, they expected certification in 2028.

As of the end of 2024, they had not agreed the full Certification Basis for their aircraft. (See page 56.) They have built 3 prototypes and are doing useful work, but they have a very long way to go.

Why is it so difficult?

eVTOL aircraft are different, and difficult.

First, they are electric powered. To date only one very small electric aircraft has been certified, so there is a steep learning curve for the companies and regulators, and Special Conditions for certification need to be agreed.

Much more complex, however, is the nature of the aircraft. Joby, Archer and Vertical all use tilting rotors for lift and propulsion. Their aircraft transition between rotor-borne flight and wing-borne, then back again when they decelerate for landing. The rotors are very small compared to a helicopter’s, but large compared to a conventional propeller on a light aircraft.

Certifying these aircraft is enormously complicated:

- Transitioning from hover (vertical lift) to cruise (horizontal thrust) is aerodynamically complex.

- Failure of a rotor during critical phases of flight can be catastrophic.

- Thrust must be precisely balanced between multiple small rotors.

- Small rotors are less efficient than large ones, requiring high power during hover – which is difficult to achieve with a lightweight battery pack.

- eVTOL aircraft with multiple small rotors can be much more prone to entering a Vortex Ring State (VRS) than similarly sized helicopters. VRS is a sudden, severe loss of lift, which is catastrophic at low altitude.

- The VRS can be asymmetric, as different rotors experience different local conditions. It can also be provoked by unexpected gusts of wind, such as are commonly experienced in urban areas surrounded by tall buildings.

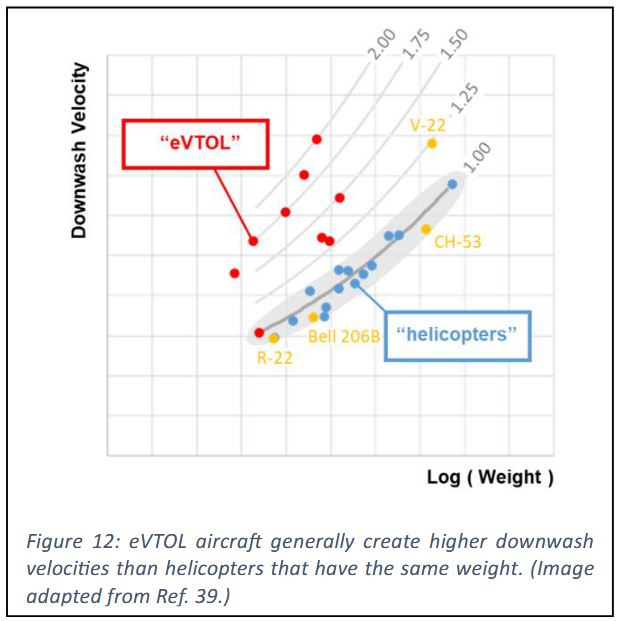

- eVTOLs create a much stronger downwash and outwash than a helicopter of similar weight, leading to higher risks to people and structures at landing sites. A study for the UK CAA stated that "[velocities that are produced by ...] eVTOL aircraft could be as much as two to three times those that are produced by conventional helicopters that have the same weight".

- All companies use ‘fly by wire’ control systems, as manual management of multiple rotors is impossible for pilots in routine operations. Moreover, the method of attitude control differs between thrust-borne and wing-borne flight. Demonstrating the safety of a fly-by-wire system in all conditions, and under all reasonably foreseeable failure scenarios, is extremely complex.

The VRS risk means that some eVTOL aircraft will not be able to follow flight trajectories that helicopters can use. It is likely that they will need to make relatively shallow approaches to landing sites, which is at odds with their intended use in urban areas. Prolonged vertical descents into restricted areas won’t be feasible because of power limitations, lack of visibility and the intense and potentially damaging downdraft that would be created.

One of the certification requirements that has been set for Archer and Joby states that “The aircraft must be capable of a controlled emergency landing, following a condition when the aircraft can no longer provide the commanded power or thrust required for continued safe flight and landing, by gliding or autorotation, or an equivalent means to mitigate the risk of loss of power or thrust.” (A recent FAA Advisory Circular uses essentially the same wording, so this requirement will apply to all 'powered-lift' category aircraft - i.e. eVTOLs.)

On the one hand, that is a fairly obvious requirement. Passengers need to be safe if the aircraft loses power. On the other hand, it is extremely complicated to meet in aircraft that cannot autorotate (i.e. make a gentle descent supported by the rotors, without power), cannot glide at low speed and don’t have a whole-aircraft parachute. There may be way it can be achieved (the "equivalent means"), but can it be done safely in an urban environment, other than by keeping takeoff and landing sites close to areas of open ground or water?

No wonder it’s taking a long time for the companies to agree their PSCPs. And do not be surprised if it takes years to complete a flight test program once the PSCPs are agreed.

Is it a problem of money?

Most startup companies developing new aircraft struggle with money, and insufficient funding obviously delays progress. But the eVTOL companies have benefited from unprecedented levels of funding from investors seduced by the vision of ‘urban air mobility’.

- Archer has raised $1.9 billion. So far it has spent about $1.8 billion (the ‘accumulated deficit’ from its SEC filings).

- Joby has raised over $2.5 billion, and spent around $1.9 billion.

- Vertical Aerospace’s total funding is unknown, but at the end of 2024 it had an accumulated deficit of £1.1 billion ($1.5 billion).

So I don’t think the slow progress is because of lack of money. Not yet, in any case - at least for the American companies (Vertical Aerospace seems less financially secure).

But eVTOL development is horribly expensive, and cash reserves can be used up quickly. There is no guarantee that any of these companies will certify their aircraft before running out of money.

A cautionary tale comes from another leading eVTOL company, Germany’s Lilium. It raised over $1.4 billion after promising commercial operations by 2025. In October 2024, the company announced that it expected certification in 2026. Then, later that month, it filed for bankruptcy.

If they certify, will they succeed?

The eVTOL companies all make bold claims about the market size.

Joby says its ambition is “to save a billion people an hour every day by delivering a new form of clean and quiet aerial transportation” (see page 1), and quote a Booz Allen Hamilton market study that says the UAM market is project to exceed $500 billion in the US alone.

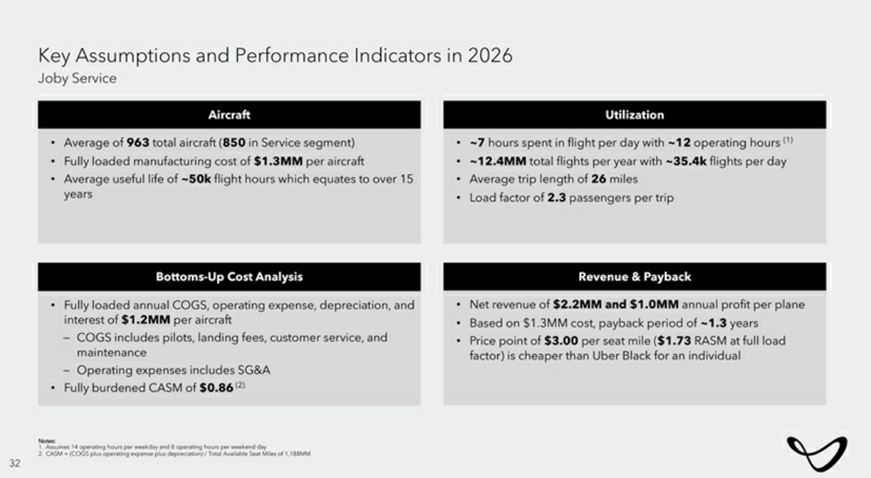

In their prospectus, Joby forecast 963 aircraft in service by 2026, costing $1.3 million each. They would, apparently, spend 7 hours a day in flight, generating $2.2 million revenue per plane, while charging less than the premium Uber Black service. They validated these very optimistic assumptions against market expectations at the time for Cruise, a self-driving taxi service. Cruise shut down its service in 2024.

The other eVTOL companies make similar claims, backed up by optimistic forecasts from Booz Allen, Morgan Stanley, McKinsey and others.

I think they are wildly overestimating the potential market size. Here are 10 reasons why I believe eVTOLs will never provide the cheap, ubiquitous, on-demand air taxi service that their developers promise:

- The aircraft will only be able to operate from a small number of ‘vertiports’ which have safe approach and departure profiles. Forget the marketing renderings showing eVTOL air taxis operating from city parks, gardens or car parks. eVTOLs will need a shallow approach path, clear of tall buildings, to minimize Vortex Ring State risks. Vertiports will need to be large enough to avoid downwash risks. They will also require fast charging infrastructure to top up batteries between flights.

- Each aircraft will need a qualified commercial pilot. In fact, if high utilisation rates are required, operators will need to hire several pilots for each aircraft. Pilots are expensive. And, before anyone asks, autonomous eVTOL flights without pilots aren't coming anytime soon! (Although Boeing, through their Wisk eVTOL subsidiary, are betting on pilotless operations.)

- Ground staff will be needed at each vertiport.

- Maintenance will need to be carried out by qualified mechanics. There is a shortage of these, which will only get worse in the next few years as experienced mechanics retire.

- Critical components may have a limited life before replacement. The danger of some mechanical failures is so high that it may be preferable to replace critical components, rather than risking degradation through wear and tear or damage through maintenance and repair by mechanics in the field. Even if manufacturers don’t want that, it may be forced on them by their product liability underwriters.

- Operators will need large numbers of aircraft if they are going to provide a true on-demand service. A passenger leaving a downtown office for the airport can hail a taxi and depart immediately. They will expect the same from an eVTOL: a fully charged aircraft ready to fly, not one that’s still inbound or waiting to recharge.

- To deliver an on-demand service, many sectors will be flown empty. This will significantly increase the price that needs to be charged on revenue-generating sectors.

- Weather conditions will limit operations. Gusting winds can increase Vortex Ring State risks. And none of the eVTOLs in development will be approved for flight in icing conditions, which will curtail winter operations in North America and Europe. It is perhaps why the companies are focusing on the Middle East market, where icing won’t be a risk.

- By the time the aircraft enter service, the eVTOL companies will have invested many billions of dollars. They will need to charge a lot to recoup their investment.

- Airspace regulations in most countries prevent low-altitude flight over built-up areas. It will take years for regulators to adapt the rules for eVTOLs, and they will rightly demand strong evidence that the aircraft can operate safely.

Conclusions

I love innovative aircraft, and I hope the eVTOL companies succeed. But I think the outlook is bleak.

- Certification is a long way off. There may even be problems that are insurmountable, and some companies might never be able to certify their aircraft for commercial use.

- The market size has been hugely overestimated. eVTOLs will be expensive, and their operation will be highly constrained, making them a niche service for a limited customer base. Not a daily time-saver for 1 in 8 of the earth’s population, as Joby claim. (I hope they will one day admit that this was a joke, despite putting it in their SEC filings!)

- eVTOLs offer little to no advantage over helicopters. Helicopters are certified, proven, and operate within established regulations. If helicopters had electric or hybrid upgrades, only noise and cruise speed would remain as potential benefits of eVTOLs. But high cruise speed matters little on short trips (and eVTOLs aren't designed to fly far), while noise would only be a critical factor if large numbers of aircraft were going to operate in populated areas.

I have focused on Archer, Joby and Vertical because as listed companies they have to declare their progress to the SEC. There are other well-funded players who can operate with less openness: Wisk, which is wholly owned by Boeing; Eve Air Mobility, which is majority owned by Brazilian aerospace giant, Embraer; and Beta Technologies, which is privately held. None of them appear to be making faster progress - although Beta Technologies is doing a lot of flying in an 'eCTOL' aircraft (Conventional Takeoff and Landing) derived from their eVTOL design.

Current eVTOL investors may see the value of their investments rise in the short term, as demonstration flights lead to speculation about future success. But the long-term outlook is bad.

Most equity analysts who follow the sector think I'm wrong. Part of me hopes that I am. I'd love a world where I could hail an eVTOL air taxi from outside my house, and I'd love to see innovative aviation startups succeed. But the evidence supports my pessimistic outlook.

About the Author: Adrian Norris

Adrian Norris is an aerospace advisor with over 30 years of international experience spanning strategic consulting, aviation and space startups, aircraft development and certification, and corporate leadership. He works with investors, founders, and executives to shape strategy, assess feasibility and risk, and distinguish real opportunities from industry hype. He was the co-founder of an aircraft development company in the US and is a licensed commercial pilot. Based in France and the UK, he holds a Master's degree in Leadership & Strategy and brings a unique blend of technical and commercial insight to the aerospace industry.

Contact

Get in touch to discuss a current project or investment.

We provide independent, evidence-based analysis to support investment and strategic decisions.